Why Most Construction Cashflow Forecasts Fail — And How to Fix Them

A systems-based approach to construction cashflow forecasting

Construction cashflow forecasting is one of those tasks everyone knows is important — and almost no one truly trusts.

Despite decades of experience, most construction cashflow forecasts still rely on simplified Excel sheets, linear assumptions, and guesswork that barely survives first contact with reality. The result is predictable: forecasts that look acceptable on paper but fail to reflect how money actually moves through a project.

After seeing this problem repeatedly across tenders, bank financing exercises, and live projects, it became clear that the issue is not effort — it’s the model itself.

This article explains why most construction cashflow forecasts fail, and outlines a more realistic way to approach them.

Where Construction Cashflow Forecasts Go Wrong

1. They Assume Detail Exists When It Doesn’t

At tender stage or early project phases, engineers are often asked to produce a full cashflow while:

The detailed WBS does not exist

BOQs are incomplete or provisional

Construction methods are still evolving

Yet the forecast is expected to look “final”.

This forces estimators to invent monthly percentages or reuse old templates — not because it’s correct, but because something must be submitted.

2. They Treat Cashflow as Linear

Many forecasts quietly assume:

“If an activity lasts 10 months, then 10% of its value is spent every month.”

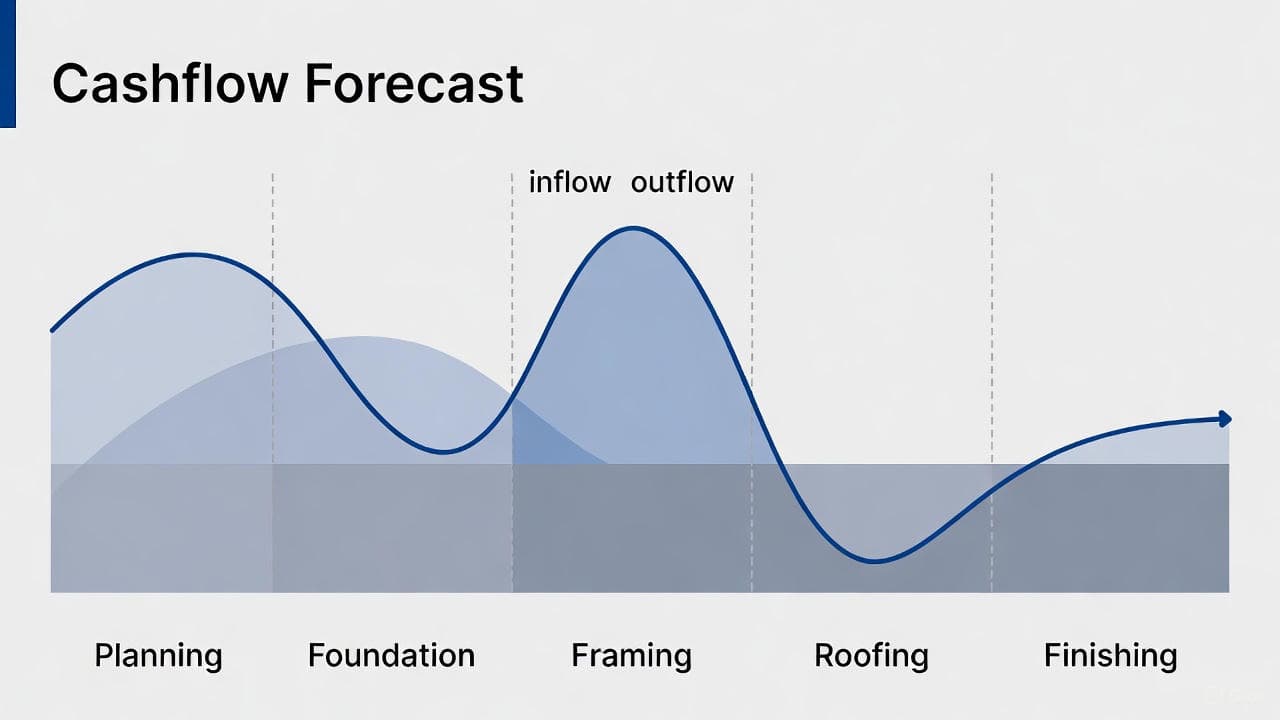

Construction does not behave this way.

Excavation is front-loaded

Concrete ramps up and down

Finishes peak late

MEP activities follow different curves entirely

Linear cashflows are convenient, but they are structurally wrong.

3. They Ignore Commercial Reality

A technically correct forecast can still be financially wrong if it ignores:

Advance payments

Retention and retention release

Defects Liability Period (DLP)

Time for payment

Work in excess of billing (WIEB)

Periods with work but no billing — or billing but no work

These are not edge cases. They define real cash movement.

4. They Confuse Precision with Accuracy

Highly detailed cashflows often look impressive — but they:

Take significant time and manpower to maintain

Break down as soon as scope or sequence changes

Are quietly abandoned during execution

In practice, a stable, high-level model often performs better than a fragile, ultra-detailed one.

A More Realistic Way to Model Construction Cashflow

A better cashflow forecast does not start with spreadsheets — it starts with what is realistically known early.

1. Start at Project Level

At early stages, the following parameters are usually available or can be reasonably estimated:

Project value

Advance payment terms

Retention and release rules

DLP

Expected WIEB

Time for payment

Capturing this logic upfront already eliminates many structural errors.

2. Use Activity-Level Abstraction (Not BOQs)

Instead of modeling:

Individual materials

Pipe diameters

Reinforcement quantities

It is often more effective to work with title activities, such as:

Excavation

Concrete works

Electrical

Mechanical

Finishes

Doors and windows

Each activity is defined by:

Start period

Duration (in periods)

Value

Optional subcontracting logic (advance, retention, payment delay)

Optional distortions (no work periods, no billing periods)

In practice, this results in:

~20 activities for small projects

~120 activities for large ones

Which is sufficient for banking, feasibility, and high-level control.

3. Model Distribution, Not Percentages

Instead of forcing linear spreads, activity values can be distributed using:

Normal distributions

Skewed curves based on activity type

User overrides where linear behavior is appropriate

This reflects how construction actually progresses — without requiring unrealistic detail.

4. Accept Uncertainty — Don’t Hide It

Early cashflows are estimates, not commitments.

A model that:

Acknowledges uncertainty

Uses reasonable assumptions

Produces consistent results

Is more valuable than one that pretends to be exact.

An Unexpected Outcome: Using High-Level Cashflows During Execution

Although this approach was designed primarily for early forecasting (tendering, bank financing, feasibility), it has also been used successfully as a final project cashflow reference during execution.

Not because it is extremely detailed — but because it is:

Stable

Understandable

Easier to maintain

On many projects, maintaining a very granular budget requires resources that simply aren’t available. A well-structured, high-level cashflow often ends up being the one management actually follows.

To be clear: this type of model generates cashflows only.

It does not handle execution follow-up, payments, or accounting — those belong in other systems. But as a reference framework, it can remain useful throughout the project lifecycle.

From Model to Tool

After seeing these issues repeatedly, I eventually implemented this logic in a small system to generate construction cashflows quickly — even when detailed breakdowns are not available.

That tool, CashflowPot by Quollnet, is essentially an attempt to encode these rules into software instead of relying on static spreadsheets.

The key lesson, however, is not the tool itself — it’s the modeling approach.

Final Thought

Most construction cashflow forecasts fail not because engineers lack skill, but because the models they are asked to use are misaligned with reality.

A good cashflow forecast:

Respects uncertainty

Matches the level of available information

Models how construction and payments actually behave

Less detail, when structured correctly, often leads to better decisions.